How close is the financial world to achieving perpetual KYC? Recent industry research has emphasised the drastic importance of improving KYC and compliance processes as financial institutions drive towards reducing the cost of a lot of the laborious, repeated, manual work being undertaken in this area. This, combined with regulators putting more and more pressure on financial institutions needing to enhance their KYC onboarding and refresh efforts, explains why perpetual KYC has become such a hot topic.

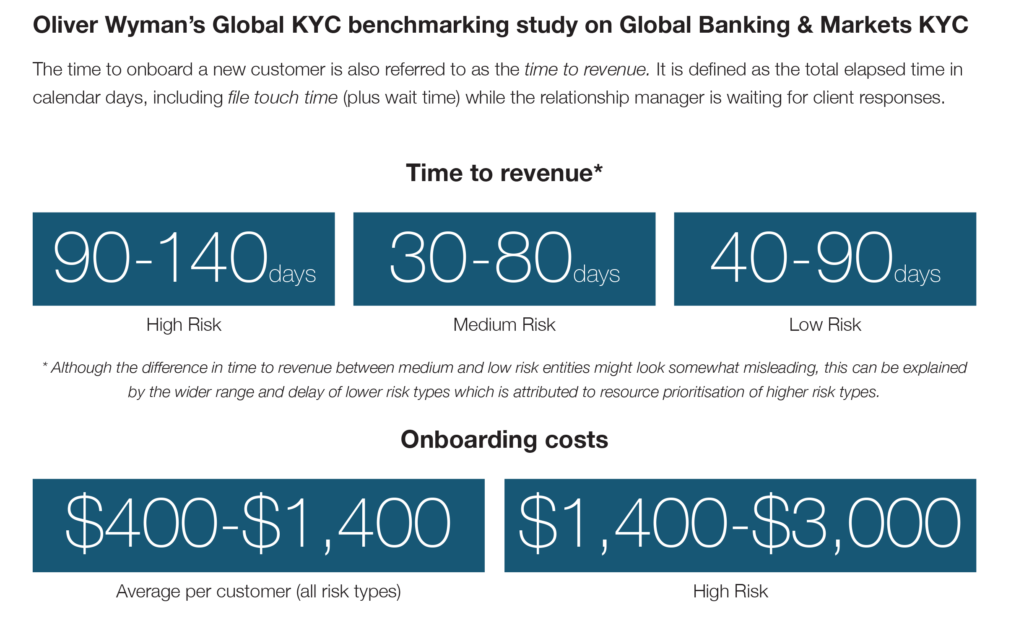

Oliver Wyman shared with us their Global KYC benchmarking study on Global Banking & Markets KYC, which has found that the overall onboarding time for corporate banking customers is a staggering 90-120 days.

For reference, one bank we work with is onboarding 6,000 new CIB customers every year but their total book of CIB customers is 240,000. Let’s assume for simplicity that 5% of a customer population is high risk, 20% is medium risk and 75% is low risk. If these files need to be refreshed every one, three or five years (depending on risk level), this means that this bank needs to onboard or refresh 70,000 customers every year.

Continuous KYC looks to minimise burdens that have troubled analysts, compliance officers and system architects for a long while. A financial institution will find that its KYC workload is split across multiple teams: customer facing front-end support, struggling to communicate effectively with the back-end data analysts. Furthermore, KYC refresh typically involves a completely manual re-do of the KYC which was conducted during onboarding or the last periodic review cycle. We commonly work with customers who have pulled together their KYC files in a manual form storing their supporting documents with written annotations in a customer folder which, for obvious reasons, makes it very difficult to share and re-use.

Besides having to deal with a disconnect between the relationship manager and the KYC analysts, KYC refreshes are further hindered by the fact that they are centered around three main pillars of data: self-reported data, external data and transaction data. In order to assess these data sets, banks currently use multiple disconnected systems and often manual processes carried out by disconnected teams.

This disconnect across an organisation contributes to out of date data and holes in the knowledge of its customers. It lowers the accuracy of a company’s customer data and their risk profiles, and increases the time it takes to complete KYC and KYC refresh.

Hence, what financial institutions need is a convergence of the three pillars of data, and a single customer view used horizontally across different parts of the organisation and systems with that information to be continuously monitored and updated. This is a level of record keeping that is yet to become commonplace, but it is clear that perpetual KYC and trigger based or event driven reviews are quickly becoming the new buzzwords in the industry, as it is finally starting to be an achievable objective.

Achieving Perpetual KYC

Download the white paper

This extract is part of our white paper on perpetual KYC. If you would like to know more about how banks can reduce onboarding times, KYC refresh costs, and improve the customer experience, you can download the full document, or feel free to book a demo with one of our team.